Your daughter's spending plan

This is the final post in my series on different ways to budget a steady income. You can hear more discussion of the different methods here on my podcast, Squanderlust.

This method is actually a digitised version of the old school ‘envelope’ or ‘jam jar’ method. Hence the name. To do this, you’ll need an account with one of the new app-based ‘challenger’ banks - Starling or Monzo. It uses their spaces (Starling) or pots (Monzo) features to manage your spending. These features are usually marketed as a way to save for goals and they can certainly be great for that, they can also be used for controlling normal monthly spending.

How to

You will need to decide what your spending types are. I suggest keeping things simple and having no more than ten. These should be a combination of your day to day spending (e.g. groceries, clothing, transport) and occasional spending (e.g. repairs, device upgrades, gifts). Both Monzo and Starling have built in categories for types of spending, which they use to label your payments out so you can see where your money is going. You can choose to base your types on their categories or create new ones if theirs don’t quite fit.

You’ll need to work out how much money you need to cover each type of expense and I talked about this in a previous post in this series. This is your spending plan. The difference in this method is how you keep track once you have the amounts worked out.

Now make a pot or space for each type of expense.

When your income comes in, sort it into the pots/spaces according to your spending plan. Monzo has a Salary Sorter function which can help with that. You’ll need to do it manually with Starling.

Monzo has a function which allows you to nominate a bill to come from a specific pot, so you can name one pot “bills” and have all your direct debits/standing orders come from this pot.

If you have a Starling account you’ll need to keep the money for bills outside of your spaces until all the bills are paid, so you will want to make sure your bills come out of your account ASAP after payday.

Alternatively you might prefer to combine this with the ‘multi-account method’ from my previous post and have a completely separate account for bills. If you want this separate bills account also to be with Starling they charge a fee of £2 a month. You may decide this is worth it to get the additional control of splitting your bills from your spending while also keeping all your accounts with one provider.

Now when you spend money, pull down the same amount of money from the relevant space or pot, so you know what you have left to spend on each area of your life.

If you need to meet an occasional expense, transfer the relevant amount from the relevant pot to the main account.

If you are extra frugal one month and have money left in your spending money type spaces/pots on pay day, transfer the extra to an occasional expense pot/space or, if these are already looking healthy, into an actual savings or investment account where you can get a good return.

Let’s talk about the advantages and disadvantages of this method.

Pros and cons

The pros:

This is a relatively low maintenance way to control spending and make sure you have enough money to cover bills and save for short term goals.

It’s more mindful than the multi-account method. If you’re spending more than you intended, you can tell fairly easily where the over-spend is coming from.

Although it’s an all digital method, this has the advantages of a cash budget method. The amounts left available for each type of expense are very clearly visible whenever you go into the app.

As with the multi-account method, as long as you err on the side of caution each time, you can be a bit rough and ready in your calculations and still be ok. For example, if you know your phone bill is typically £17-20 then as long as you leave £21 in your bills account/pot for it, you know you will be ok.

You are almost certainly never going to get a charge for a bounced direct debit or an unpaid bill.

While you’re out and about, you can tell straight away if you can afford to treat yourself now or if you’ll need to wait. No need to consult your spreadsheet.

Very easy to sustain. If book-keeping style budgets don’t work for you and become overwhelming, this will almost certainly be a better choice.

Don’t have to remember to request/keep your receipts.

The cons:

May need to switch banking providers, which can have an impact on your credit record.

Takes time to set up.

Need to be comfortable with app-based banking.

Need to spend time moving money between the pots.

Need to be sure any automations are working correctly, have the right amounts and come out on the right days.

Unless you create a single “occasional spends” pot/space, you may find you need to pay for a particular item before you have saved enough e.g. if the washing machine breaks suddenly. This might mean you have to transfer between the pots/spaces for this type of spending to make up the difference.

What do you think? Would this style of spending plan work for you?

To hear more about different ways to plan and track spending, check out my podcast Squanderlust Episode 7 : Budget Pick ‘n’ Mix

The multi-account method

Today we’re going to get into budgets for people who really hate the admin side of budgeting. This is a way to automate parts of the control of your spending and make certain you have money ringfenced for bills and savings before you can spend anything.

How to

For this method you need three accounts, two basic or current accounts and one instant access savings account. The first current or basic account is for bills and other automated payments. this needs to have direct debit/standing order facilities. The other basic/current account is for spending money and it needs a debit card. The instant access savings account is for keeping money ready for occasional spending - things like birthdays, household or car repairs and religious festivals. It may be useful if this is with the same bank or building society as the spending account, so you can easily transfer between them.

You’ll need to work out how much money you need to cover all your expenses and I talked about this in a previous post in this series. The difference here is how you keep track once you have the amounts worked out.

Ideally, you should get income paid into your bills account. You will need to know how much needs to stay in this account to cover your bills until next payday. I suggest you keep back a little bit more than this amount, in case any of the bills is higher than expected.

Then decide what needs to be paid into your savings account to cover the occasional costs. If this will be a consistent amount, you can set up an automated payment to the savings account. Alternatively, you can make the transfer manually on the day you get paid.

Decide how much you want to go into longer terms savings and investments and, ideally, automate these transfers too, then you can treat them like a bill.

Finally, transfer the amount you want to use for day to day living expenses into your spending account.

If you need to meet an occasional expense, transfer the relevant amount from the instant access saver to the spending account.

You’ll need to keep an eye on how much is left in your spending account throughout the month. You should also schedule some time once a week/month to go though your bank statements/online banking. That way you can be sure that there are no unexpected payments and that the amounts you have going into each account are still appropriate.

If you are extra frugal one month and have money left in your spending account on pay day, transfer the extra to the occasional expense savings account.

Let’s talk about the advantages and disadvantages of this method.

Pros and cons

The pros:

This is a low maintenance way to control spending and make sure you have enough money to cover bills and save for short term goals.

Although it’s an all digital method, this has many of the advantages of a cash budget method.

As long as you err on the side of caution each time, you can be a bit rough and ready in your calculations and still be ok. For example, if you know your phone bill is typically £17-20 then as long as you leave £21 in your bills account for it, you know you will be ok.

You are almost certainly never going to get a charge for a bounced direct debit or an unpaid bill.

While you’re out and about, it’s very easy to see at a glance if you have spare fun money this month, or if you need to tighten your belt. No need to consult your spreadsheet.

Very easy to sustain. If you’re someone who has started multiple book-keeping style budgets in the past and never kept up with them after the first couple of weeks, this willll almost certainly suit you better.

Don’t have to remember to request/keep your receipts.

The cons:

Less likely to spot a fraudulent payment quickly.

Need to be sure your automations are working correctly and come out on the right days.

Less familiar with the nitty-gritty of your spending, so less likely to spot opportunities to save money, without additional effort.

Requires multiple accounts, probably with at least two different providers.

What do you think? Would this style of spending plan work for you?

To hear more about different ways to plan and track spending, check out my podcast Squanderlust Episode 7 : Budget Pick ‘n’ Mix

Book-keeping-style spending plans

Today I’m going to talk about the type of spending plan that most people mean when they talk about a “budget”. That is to say, a list of sources of income and a list of types of expenses and payments to savings/investments with weekly or monthly amounts of each beside them, so you can add up each list and check they balance. Actual income and spending is then tracked against the lists to make sure you’re not going outside your plan.

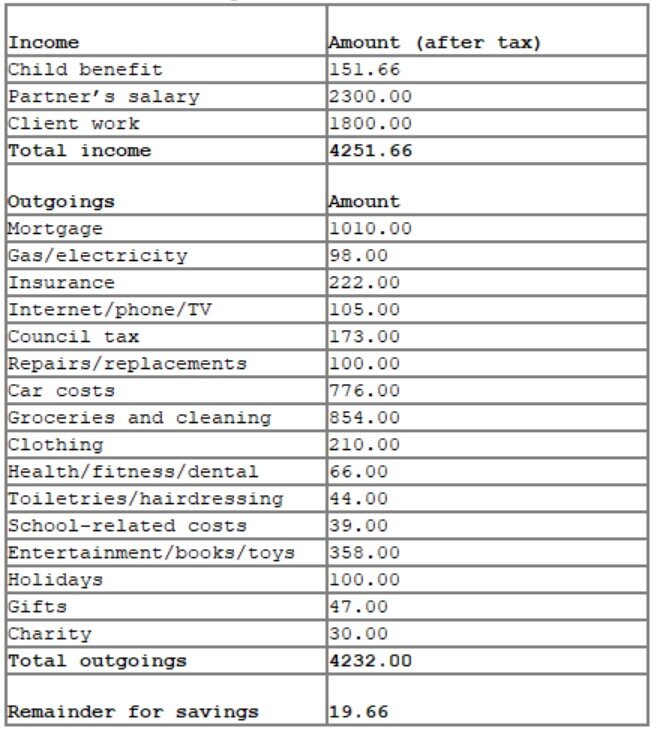

Let me give you an example. This is a plan for two parents on a moderate income with two kids and in a rented three-bedroom house with two cars to run and no pets.

Leaving aside the actual amounts here*, let’s talk about the advantages and disadvantages of this method.

Pros and cons

The pros:

You know exactly, and I mean exactly, what’s going on with your money at any given time.

You can catch any risk of overspending immediately before it happens.

You can spot fraudulent payments and rising costs immediately and do something about it.

The cons:

Time consuming - this is the biggest one, it takes time and effort to set up and then time to maintain.

If your spreadsheet or app goes wrong somehow, then things can get very frustrating.

You need to be consistent with it and build it into your routine.

May need to get into the habit of asking for/keeping receipts or you’ll have unaccounted spends which can quickly pile up.

If you think this method could be for you, here’s how you create a plan this way and make it work.

How to

You can do all the calculations on paper, but it’s easier with a spreadsheet and most spreadsheet programmes come with personal or family budget templates galore. There is also one on Money Saving Expert, StepChange and honestly, practically every money blog out there. You can also make your own. Alex did after we recorded this episode of Squanderlust and you can find out how she got on in this episode. I used to use this template, but I don’t use this method personally, any more.

If you’re going to build your own spreadsheet, you need to know what calculations need to go into it, so let’s talk about that. If you hate maths and will be using a template, you can skip this, but I promise it’s all very easy maths.

Weekly or monthly?

The first thing is that your spending plan needs to be for either weekly or a monthly spending. There isn’t a hybrid method. Weekly makes it easy to track smaller amounts of money and day-to-day spending. Monthly works better for bigger overall amounts, monthly salaries and bills paid by direct debit/standing order.

Our spending, however, usually comes in a mix of weekdays, daily, weekly, monthly and longer time periods. So we need to do some conversions.

To convert to weekly:

= weekday spend x 5

= daily spend x 7

= monthly spend ÷ 4.33 (because there are 52/12= 4.33 weeks in a month, not 4)

= quarterly spend ÷ 13

= annual spend ÷ 52

To convert to monthly:

= weekday spend x 21.66 (because 21.66 = 5 x 4.33)

= daily spend x 30.32 (because 30.32 = 7 x 4.33)

= weekly spend x 4.33

= quarterly spend ÷ 3

= annual spend ÷ 12

I don’t wanna do maths or spreadsheets

That’s fine, there are loads of online calculators that do this for you. Two examples that come to mind straight away are The Money Charity’s Budget Builder and the Money Advice Service Budget Planner. There are lots of great phone apps that do it too, but we’ll leave those for another day. You can also do a different style of spending plan altogether.

Make it accurate

I can’t emphasise this enough, your plan must be based in reality. If you fudge it you won’t be able to stick to it. How do you make it accurate? Look at the actual figures. Use bank statements, receipts, payslips, benefits entitlement letters, bills and so on to work out how much money actually comes into your household and where it goes.

This is often the point where people give up from sheer shock at the real numbers, which can seem very discouraging. They don’t have to be though. They’re your starting point, not your end point.

You can set targets to change the numbers as part of your plan. If you realise you’re spending more than you thought on energy, you can look at ways to cut your electricity bills. If you’re spending way over the odds on your phone tariff, that’s something you can switch up. If your grocery bill is twice what you thought it was, you can research tips on thrifty meals and avoiding food waste.

A note on occasional spends

One thing that wrongfoots people doing this style of spending plan is occasional spends. Birthdays, Christmas and other religious festivals, household repairs, replacement gadgets, school uniforms and trips, new tires and the like all need to be in your plan or you will never have the money for them and you’ll always feel like you “can’t budget because something always happens”. If they’re in the plan, you can put money aside for them each month. Build up a pot of cash in an instant access savings account ready to cover them. Work out what you expect to spend on each of these types of costs every year and treat like an annual cost as above.

Balance your budget

This is the moment of truth, when you add up all your expenses and take that away from the total of your income sources, what do you have left? If there’s money left over, happy days, you can put that towards saving and investing for your future. If not, then at least you can investigate where the issue is and look for fixes. If things are looking very bleak, don’t delay contact a debt adviser. If the idea of that feels uncomfortable, we talked about why it’s good to get advice early on the podcast, including a description of what happens when you go for debt advice, so you know what to expect.

Once you’re happy you’ve got your outgoings below your income and enough going towards your future needs and wants, take a moment to admire your plan. Congratulations on your hard work.

Wait there’s more!

Lots of people get this far and then stop, but I’m afraid this is the beginning not the end. A plan is pointless if you don’t act on it. Now you need to actually track your income and spending against your plan. It’s usually best to do this daily, or at least every other day. Miss this step and the whole ‘making a spreadsheet’ bit was a waste of time. You need to actually make sure you spending no more than you planned and that your allowances for your different categories were appropriate.

Once you start tracking, you might find that your plan was a bit out here and there. It’s pretty common to get it wrong the first time. That’s ok, you can adapt and update it as necessary. As you get better at finding ways to be thrifty, you can start putting more towards paying down borrowing or into savings and investments. Or, if you’ve been being a bit over-frugal, you can re-introduce some fun and creature comforts into your life, safe in the knowledge that you can afford them, because they’re in the plan.

(*this family could probably save loads on some areas and other areas the figures might be unrealistically low)

Would this type of spending plan work for you? What do you think?

To hear more about different ways to plan and track spending, check out my podcast Squanderlust Episode 7 : Budget Pick ‘n’ Mix

Mix it up with the cash combo spending plan

Last time I talked about the all-cash spending plan and the pluses and minuses with it. The most obvious minus is that paying bills in cash often incurs extra charges and is a giant faff.

Introducing the cash combo plan. All the convenience of electronic payments, just as tangible and intuitive as the all-cash plan.

Here’s how it works. You set up automated payments for all your bills, savings, insurances, and credit repayments. Make sure there’s enough in your current account to cover these each week/month, plus a little bit of extra, in case any of the bills is higher than expected. Then you withdraw the money for your spending including both essentials like groceries and more fun things like renting a movie.

You can treat the cash like you do for the all-cash plan, sorting it into envelopes for different types of expenses.

You’ll probably need more envelopes than this, especially if you have children.

Alternatively you can just have two envelopes, one for “essentials” and one for “non-essentials”. The key is to be over-generous with the “essential” envelope and not take money out of it, except for your those essential expenses, until you get to the end of the week/month. The one downside with doing things this way is you’ll know less about where your money is going than with the “types of expense” version.

Two nice, big, fat envelopes. More simplicity, less control.

At the end of the week/month if there’s still money in the “essential” envelope, you can decide whether to put it back into a savings/investment account or to treat yourself.

One thing to bear in mind is that because bills are easier to manage on a month by month basis but spending is easier to manage on a week by week basis, you may also choose to withdraw your spending cash weekly or to withdraw for the month, but have weekly envelopes.

You do know only February has four weeks, right?

So, what do you think? Would you find the cash combo spending plan useful?

For more on different ways to create a spending plan listen to my podcast, Squanderlust.

Going old school with your grandma's spending plan

Our first way to craft a spending plan (or budget, if you must) is the most low-tech way imaginable. This is a method that people used for centuries. Before there were debit cards and challenger banks and smartphone apps there was the all-cash spending plan. Your grandma or great grandma may well have used a system like this and with good reason. It’s simple and it works.

This way of planning spending has a few other names. People also call it the cash diet and, for reasons that will become apparent, the jam jar method or the envelope method.

Here’s how it works.

Take all your money for bills and spending for the week or month out of your account. Transfer the money you’re putting aside for future savings and investments into the relevant accounts.

Label a set of containers with the expenses you have to pay (fuel, water, food, clothes, children’s activities etc). Envelopes or jam jars are the classics, but a set of ziplock bags will work, or the zip-up pockets in a personal organiser.

Share your money out between the containers. Start with the most important bills i.e. housing costs, fuel, TV licence, council tax, and work down. Only spend from the correct containers, try not to swap money between them. Do not take money out of the containers for covering bills to pay for other costs. Have one container for emergencies and add to it each month. Wanting a bottle of wine is not an emergency.

Pros and Cons

This is a straightforward system and it can’t be fudged. The money is either in a container or it isn’t. This makes it a very tangible, intuitive system for people who struggle with focusing on the numbers on a screen or connecting them to their real life purchases. If your maths is a bit iffy, this requires much less calculation than other systems. You just share out the cash until everything is covered.

It’s also great if you have had a tendency to tell yourself it’s ok to overspend because you’ll “make it up later… somehow”. It makes it very clear there is no making it up “somehow”. The only way to make it up is to cut down spending on something else.

Of course, there are downsides. Most of us don’t want to pay all our bills in cash, even if we have the option. Automated billing saves a lot of time and effort and as long as the money’s there, you know your payment won’t be late and affect your credit score. Moreover, there are obvious security risks to keeping lots of cash in your home and most of us want to avoid those.

We’re moving to a cashless society and some shop assistants will look at you sideways if you pay cash, especially for bigger ticket items. They may think you’re involved in some kind of shady activity and trying to launder the money (although, for real, no one launders money that way, not efficient enough for the sums involved).

Depending on where you live there may not be a cash machine local to you, so making the weekly/monthly withdrawal may take planning. No one wants to spend extra on travel just to get their money if they can help it.

Still this is a solid way to plan weekly or monthly expenses for anyone who wants to get a really tight rein on their spending.

What do you think? Is this something you would ever try?

To hear more about different ways to plan and track spending, check out my podcast Squanderlust Episode 7 : Budget Pick ‘n’ Mix

The pros and cons of budgeting

Ugh… budgeting.

No one wants to, we all know we “should”, and if you read any personal finance blog you’ll be told you must, because it’s the foundation of good financial management. There will probably be the classic quote from Mr Micawber, the literary patron saint of debtors:

‘My other piece of advice, Copperfield,’ said Mr. Micawber, ‘you know. Annual income twenty pounds, annual expenditure nineteen nineteen six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds nought and six, result misery.”

David Copperfield (1850) by Charles Dickens

This is true enough. Money out must be less than money in, or it all goes horribly wrong.

Even so. Ugh…. Budgeting.

One reason, I think, why the personal finance experts who urge us all to budget can come across a bit… dare I say, preachy, is because they only acknowledge the upsides to planning and tracking your expenses. Many don’t like to mention the reality that there are downsides too.

Now in my opinion the downsides are more than outweighed by the upsides, but it’s disingenuous to pretend they don’t exist.

So I’m going to be really frank and give you the pros and cons and you can decide for yourself.

First the downsides.

It’s boring. Simple really. There are lots more exciting and interesting things we could be doing with our time than tracking our spending. Some people get really into it and good for them, but, in general, it’s a chore. Most of us don’t want to make admin our hobby.

It takes time. Related to 1. is the fact that there are only so many hours in the day and many other activities, not to mention people and pets, that want our attention. You may also have planned to spend quality time with kids, partners and friends, stay hydrated, exercise, meditate, keep up with hobbies, read enough of the news to have semi-informed opinions about the world and maybe, I dunno, do whatever your employer or customers pay you to do. Adding in time to plan and track your spending can feel like the final straw for an overloaded schedule.

It can be depressing. If you’re used to just crossing your fingers and getting by on hope, reality can bite hard when you finally face it, and creating a spending plan means you do have to face reality. There’s no point in writing a plan that isn’t based in fact. This is one of the biggest hurdles to a lot of people’s budgeting. They just don’t want to know how bad things are.

It can cause regret. There’s nothing like making a positive change, to make you regret not having changed sooner. Especially when it comes to stopping overspending and starting to save and invest. It brings you up short against all the ways you’ve wasted money that could have gone on a better financial future.

No spending plan, no need to feel those pesky regrets today. Ta da! (never mind that they’re waiting around the corner.)

Maths. (I mean, it’s only basic arithmetic and there are lots of apps and spreadsheets that will do it for you but still… I know anything to do with numbers bothers a lot of people.)

You may have to give up on some of your pleasures. This is another big one. It’s easy for us to convince ourselves that things we want are in fact “necessities” or that we just can’t save “this month” but we will next month when we’re magically better people who don’t shop so much and buy fewer takeaways.

A spending plan makes it clear how much we can actually afford to spend on shopping and takeaways (or e-books and in-game purchases or whatever tends to tempt you). There’s no getting away from it, something will have to give and it’s probably some of your fun money. Do. Not. Want.

OK, that’s enough downsides. If I’ve forgotten any, tell me in the comments.

Let’s look at the upsides

You know exactly where you are. This is key. Knowledge, as they say, is power. Without a plan you’re constantly guessing about whether you can afford the things you need or want. The truth is you’re probably making mistakes all the time.

Do you have enough money for that day trip? …maybe… If you go, will you have enough for your friend’s birthday present at the end of the month? … you hope so…

With a spending plan you can answer those questions. You can go on the day trip as long as it doesn’t cost more than £45, that way you’ll still have £20 for your friend’s present.

You can find relatively painless ways to save. A spending plan can be a great motivator to switch up your utility, credit and insurance providers so you can find more money for fun and savings. With a plan you can see straight away how doing this will benefit you.

You can get greater value from your spending. It may be that you’re spending on non-essentials in ways that are costing more than you realised and don’t actually bring you joy. Having a plan will show you what’s really going on and help you focus your spending on what you value most and away from the trivial.

You can spot frauds, errors, and price increases straight away. If you’re tracking your spending and bills every month against your plan, then you’ll notice if something doesn’t add up. The minute your mobile phone company increases your bill, you can find a new plan. If there’s a payment you don’t recognise, you can query it. If you’re charged twice for the same thing you can request a refund. Giving money away for no reason? No thanks!

You can plan to pay occasional expenses out of savings, not credit. Household repairs? You can put the money aside for that. Birthday and other celebrations? They’re in the plan. School uniforms? Covered. A nice meal on your anniversary? Heck, yeah!

Even if something essential is more than you thought ("New brakes to go with that MOT, Madam?") and you have to shuffle money out of, say, your holiday fund, or even put the difference on a credit card, you’re still better off than if you had no plan at all and needed to find the whole sum out of nowhere.

If you need to say “no” to a pushy salesperson or a whining child, you can do so assertively, because you’re clear about what you can afford and what you can’t. You can also say “not yet” if you will have the money later on, which brings us to the next upside.

If you have children, you can set a good example and help them learn positive money habits. By telling your children “we don’t have the money for this yet, but we’re saving up” you’re encouraging them to do the same for the things that they want.

You can build an Emergency/Rainy Day/ F*** Off Fund. Start with saving one month’s basic expenses, then build up to three months and eventually between six months to a year’s worth. Then if you can’t work or you have a sudden big expense, you’ll know you’ll be ok.

You’ll be surprised what you can afford. Remember the day trip in point 1? Without a spending plan you might assume you couldn’t afford to go because of your friend’s birthday and then you’d miss out.

What’s more, planning spending allows you to save for goals that may previously have seemed completely out of reach. These could be things like a good camera and a set of fancy lenses, a really gorgeous winter coat, a high-powered laptop, or a super-comfortable new sofa.

You can give more. When you know what you have and you’re confident you can afford what you need, then it’s nothing to give some of your non-essential spending money to a cause you believe in. I personally love Money A + E, a black-owned community organisation helping BAME and vulnerable groups to improve their financial wellbeing through advice and education. You can hear an interview with their founders here.

You can start to invest more for the long term. Once you are in the habit of using your plan to find ways to save, you can put some of those savings into investments, whether through an ISA or pension to grow your wealth and make your future self richer.

You’ll have peace of mind. It’s stressful not knowing what’s happening with your money. You constantly carry the fear of not knowing what you’d do if your income dropped or you faced a sudden expense. A spending plan gives you clarity. You know where you are so you can see what actions you need to take and nothing is more reassuring than that.

So there you have it, the pros and cons of creating a spending plan. I definitely think it’s worth the effort, and I believe me I had to get over every one of these downsides to feel it. The last upside is the kicker.

Peace of mind is, frankly, priceless.

The question is how to make a spending plan that actually works for you. I’ll be writing more blogs about that, and you can also listen to Alex and me discuss it on my podcast, Squanderlust.